In a previous article I pointed out that the marginal cost of gold production including exploration, feasibility studies, construction, maintenance, production and taxes has doubled since 2009 up until now. That has placed a large burden on gold mining companies over this period. The result was a decline in the gold mining index (GDX) of around 10% since 2010. Even when the gold price steadily went up from $800 to $1600/ounce, there wasn't a lot of profit to be made by the gold mining companies themselves. This means that gold mining companies are very dependent on the gold price for their margins and profits. At the same time, I want to make a case that the gold price is also very dependent on the mining companies.

If anyone ever says that gold mining production isn't going to affect the gold price, you can use these charts to prove them wrong.

In 2012 we had 4000 tonnes of total gold supply per annum, while gold mine production was around 2812 tonnes per annum in 2012. That's a 70% interest of gold mine production as compared to the total gold supply.

If the gold miners continue to have lower prospects for production due to the marginal cost of production rising above the gold price (total marginal cost is currently $1500/ounce), then the supply of gold will drop. As a result we will see a rising effect on the gold price when this supply breaks down.

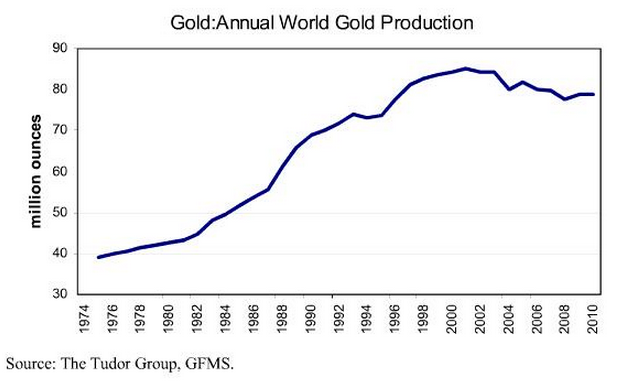

Mine supply had been going up since 1974 (Chart 1), but has peaked since year 2000. I believe mine supply is going to stay flat or even drop going forward due to decreasing ore grades and higher marginal costs of production.

To read more, go here.

Geen opmerkingen:

Een reactie posten